How Interest Rate Movements Impact Private Credit Valuations

Interest rate movements aren’t just background noise - they directly influence the fair value (“FV”) of private credit portfolios.

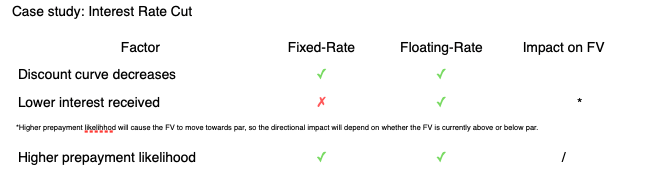

Discount rate dynamics

A key input into fair value is the discount rate applied to future cash flows. When risk-free rates rise, the discount curve shifts upward, reducing present values. When rates fall, the discount curve shifts downard and valuations typically rise.

Funds must ensure their discount curves are updated in line with observable OIS or government yield data to avoid stale valuations. Additionally, in practice, credit spreads also change with macro conditions - this can offset or amplify the impact of movements in the risk-free curve.

Floating rate loans: the double-edged sword

Floating-rate loans provide natural protection against rising rates, as interest income increases automatically. But that same dynamic can increase stress on borrowers whose debt servicing costs spike, raising expected default risk.

Funds often use interest rate caps, collars, or hedges to manage this exposure, and floors to prevent yields collapsing when rates fall. Valuations should reflect these embedded features, especially when market expectations on rates shift.

Prepayment and refinancing risk

Falling rates make refinancing more attractive to borrowers, increasing prepayment risk. For lenders, this shortens expected duration, lowers realised IRRs, and creates a potential need to reinvest at lower yields.

To mitigate this, funds may include prepayment penalties or make-whole clauses, but valuations should incorporate the probability-weighted prepayment scenario.

Floating or Fixed: Why the Impact of Rates Isn’t the Same

Key Takeaway:

As base rates shift, credit funds should regularly calibrate discount curves and borrower risk assumptions to ensure that valuations remain accurate.