Fair Value Matters: Why Funds Can’t Afford to Stand Still

In private markets, “cost” is rarely the same as “value.”

While cost reflects what was paid, fair value reflects what it’s worth today - and for investors, regulators, and auditors, that distinction is critical.

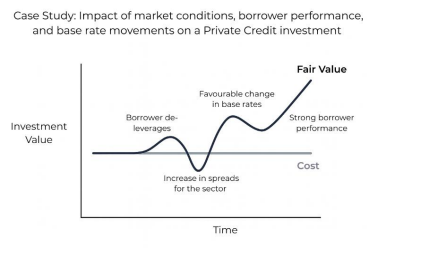

Cost is static - markets aren’t.

Private investments evolve rapidly after acquisition. Performance, leverage, market conditions, and comparable transaction multiples all shift - often within months. A cost-based approach ignores these dynamics, masking both gains and impairments.

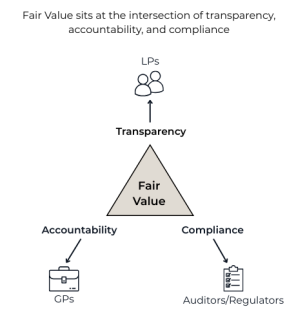

Fair value brings transparency.

Limited Partners (LPs) rely on timely, unbiased valuations to assess fund performance, portfolio risk, and capital efficiency. Fair value marks enable comparability across funds, vintages, and asset classes - critical for asset allocation decisions.

It’s not just best practice - it’s required.

Accounting standards such as IFRS 13 and ASC 820 mandate fair value measurement for investments held by funds. Meanwhile, the FCA has recently increased scrutiny on private market valuations. Regulators and auditors expect periodic, supportable valuations that reflect observable market inputs wherever possible.

Cost can mislead.

A portfolio marked at cost can overstate NAV in downturns and understate it in growth markets. For LPs, that distorts IRR, risk metrics, and ultimately, trust. Funds that adopt consistent, data-driven valuation frameworks not only satisfy auditors - they build credibility with investors and accelerate fundraising cycles.

Conclusion:

Regular fair value measurement provides a transparent view of portfolio performance, ensuring investors, auditors, and regulators can assess risk and return with confidence.