Valuing the Unlisted: How to Approach Illiquid Equity Valuations

Fair value isn’t guesswork - it’s a disciplined process built on market evidence, calibrated models, and informed judgement.

Defining Fair Value

Fair Value (“FV”) under IFRS 13 is “the price that would be received to sell an asset in an orderly transaction between market participants at the measurement date.” Unlike book values or historic cost, FV reflects current market participant assumptions - even when no observable price exists. For privately held equity, this means estimating what a willing buyer would pay today for the same stake.

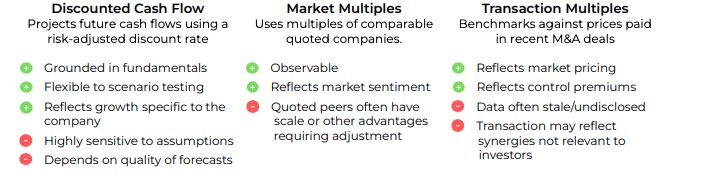

Core Valuation Approaches

In practice, most valuations blend these methods: using DCF as an anchor (provided there are high quality forecasts), and market/transaction multiples to sense-check or calibrate results. There are several key judgements to be made for each of these approaches. We will delve into the specifics of each of them in a separate report.

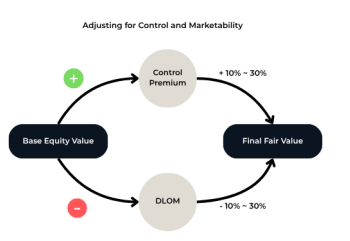

Adjusting for Marketability and Control

Even after estimating enterprise and equity value, the characteristics of the specific stake being valued can materially impact fair value. Discount for Lack of Marketability (DLOM): Reflects the illiquidity of the holding and the expected time required to realise value through an exit. Typical discounts range from 10% to 30%, depending on market depth, volatility, and expected holding period.

Control Premium: An upward adjustment applied when the interest being valued conveys operational control or majority voting rights, recognising the ability to Valuing the Unlisted: How to Approach Illiquid Equity Valuations influence strategy, capital structure, and distributions. This is also typically in the range of 10% to 30% depending on the extent of control.

Calibration and Cross-Checking

For funds, calibration on a regular basis is key. Valuations at entry (cost) should be periodically tested against actual performance, peer multiples, and exit markets. The fair value should evolve as visibility improves - not remain static. Consistent methodology, transparent assumptions, and a balanced approach uing different methods support auditability and investor confidence.

Key Takeaways:

• Fair value ≠ intrinsic value; it reflects market participant pricing

• Combine methods - no single model captures the full picture

• Adjust for liquidity, control, and minority characteristics

• Calibrate continuously against observable market data