The Myth of Par: Why Private Credit Loans are Rarely Worth Face Value

In private credit, par is often treated as the valuation conclusion by default, when it should instead be a reference point.

In private credit portfolios, loans are often reported at or close to par while they continue to perform. Interest is paid, contractual terms are broadly observed, and no obvious credit event has occurred. In that context, holding value at par can feel reasonable and, in many cases, prudent.

However, par reflects the contractual face value of the loan rather than a valuation mark. Fair value, by contrast, reflects the price that would be achieved in an orderly transaction between market participants at the measurement date. While the two can align, they should do so as an outcome of underlying fundamentals rather than by default.

When a performing loan may be worth more than par

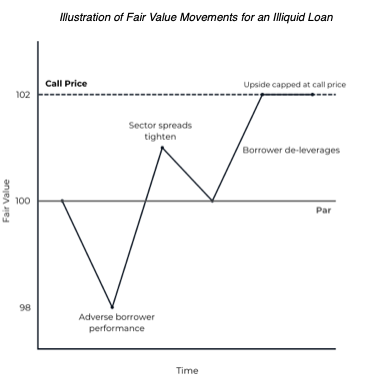

Par is not a ceiling. If market yields for comparable instruments compress after origination, or the borrower’s credit risk improves, the terms of the loan may become more attractive relative to pricing for new issuances. In such circumstances, a third-party buyer may be willing to pay a premium.

In practice, upside is often capped by call protection; for example, where a loan is callable at 102% (par plus a 2% prepayment fee), fair value is naturally constrained around that level, as pricing materially above it would incentivise prepayment.

When a performing loan can be worth less than par

A loan does not need to default to trade below par. Even where contractual payments remain current, value may fall below par due to:

A shift in the market price of risk, reflected in wider spreads or higher yields across comparable instruments

Higher leverage than when originally underwritten

Reduced liquidity headroom or a deterioration in cash flow visibility of borrower

Deterioration in sector fundamentals or sponsor dynamics

Changes to loan’s cash flow profile (e.g. alteration of the repayment or drawdown schedule)

In each case, the borrower may continue to perform, but a market participant would require a higher return to hold the loan, which would be reflected in a lower fair value.

Amend-and-extend as a valuation inflection point

An increasingly common feature of the current private credit market is the use of amend-and-extend transactions, where loan maturities are extended rather than refinanced or repaid at the original maturity, typically reflecting tighter refinancing conditions. When a loan’s maturity is pushed out, expected cash flows are deferred and the lender is exposed to a longer period of uncertainty, even if the borrower continues to perform.

While additional fees or margin increases may partially compensate for this, they do not fully offset the impact of increased duration and reduced exit options. From a valuation perspective, this typically warrants a reassessment of fair value through a higher required return, a longer weighted average life, or both. Whether this results in a movement away from par depends on the balance of those factors, but the extension itself represents an economic change that should be explicitly reflected in valuation.

Why par persists in practice

There are practical reasons why par remains prevalent in private credit valuations. The loans are illiquid, observable transaction data is limited, and valuation processes are often designed to promote stability and consistency in the absence of clear pricing signals. Moreover, the absence of realised losses or indicators of default is often interpreted, implicitly or explicitly, as confirmation that the value of the loan is unchanged.

Nevertheless, fair value is not contingent on loss events. It reflects how market participants would assess risk and return at a point in time, given current information.

Conclusion

Par should be a fair value mark supported by analysis, rather than the default assumption. Holding a loan at par can be appropriate where risk, duration and lender security remain broadly unchanged from origination. In practice, however, those factors often evolve, meaning fair value is unlikely to remain exactly at par even when the loan continues to perform.

This is not an argument for excessive valuation volatility. It is an argument for applying consistent valuation judgement as credit risk evolves over time. Par may be a reasonable outcome, but it should not be maintained by default.