How Interest Rate Movements Impact Private Equity Valuations

Shifts in base rates can meaningfully reshape private equity valuations.

Generally, lower rates support higher enterprise values (“EV”) through lower discount rates, lower interest costs, and greater investor appetite. Higher rates have the opposite effect. Understanding how these dynamics flow through the two main valuation approaches - the income approach and the market approach - is key to producing defensible valuations aligned with current macro conditions.

1. Income Approach (DCF): How base rates flow through to EV

Discount rate (WACC)

Interest rates feed directly into the risk-free rate, which drives both the cost of equity and expected cost of debt. When rates fall, the discount rate declines and the present value (“PV”) of future cashflows rises; when rates rise, valuations compress. Because the discount rate affects every projected year, it is typically the most rate-sensitive input in a DCF.

The terminal value (“TV”) often represents over half of total EV. Because it represents cashflows far into the future, even small changes in the discount rate or long-term growth assumption can move the TV materially.

Interest Costs and Refinancing assumptions

Many PE buyouts use floating-rate debt, so changes in base rates feed directly into cash interest costs. Lower base rates reduce interest expense and lift free cashflow during the forecast period; higher rates do the opposite.

Even when the debt is fixed, movements in base rates will affect the expected cost of debt for future refinancing, which will feed through to the TV. Additionally, any refinancings within the forecast period would need to factor in the amended base rate.

Operating and working-capital effects

Rate environments influence business performance indirectly. Cheaper financing can support investment, inventory funding, and demand, while higher rates may constrain capex or extend working capital cycles. These changes flow through to forecast cashflows.

2. Market Approach: Why multiples move

Financing conditions

Base rates shape public-market valuation levels. Lower rates and tighter credit spreads reduce discounting and increase investor risk appetite, lifting comparable EV/EBITDA multiples. When rates and spreads rise, public-market multiples compress as discount rates increase and risk appetite weakens.

Buyer appetite and competition

When rates are low and credit is abundant, more sponsors can finance acquisitions, increasing bidder participation and supporting higher EV/EBITDA multiples. When credit tightens, fewer buyers can raise debt, reducing competition and moderating entry multiples.

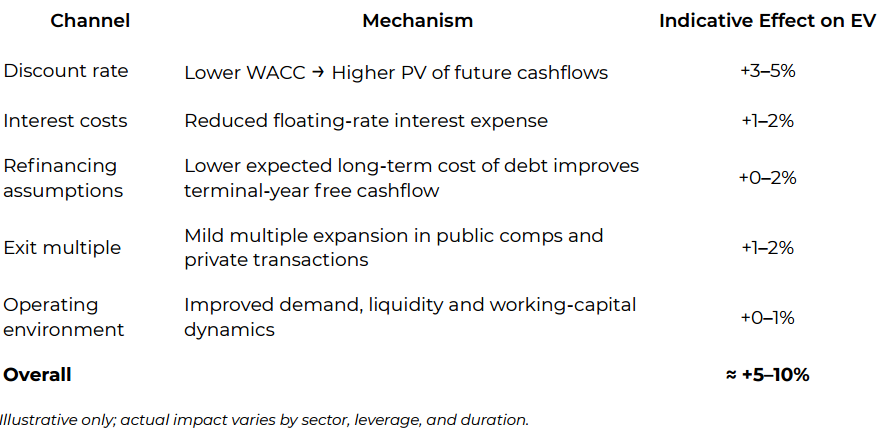

3. Illustrative impact of a 50bps rate cut

Key Takeaways

Base rate movements affect private equity valuations through two main levers:

1. Discounting and refinancing dynamics within DCF models, and

2. Financing conditions and market multiples in the transaction market.

Even modest rate shifts can move EV by several percentage points. In order to ensure that their portfolio valuations remain current, funds should:

• Re-anchor WACC and TV assumptions to current yield curves

• Refresh public-market comparables regularly

• Consider amending refinancing assumptions